Fed Finally Hikes. Mortgage Rates Fall. Wait... What?!

Last week I said that the Fed had done a great job of making sure markets were fully prepared for the upcoming rate hike. That’s no great mystery, but it is something that needed to be seen to be truly believed. Markets were so prepared, in fact, that mortgage rates moved lower on the day of the Fed rate hike, and substantially lower the following day.

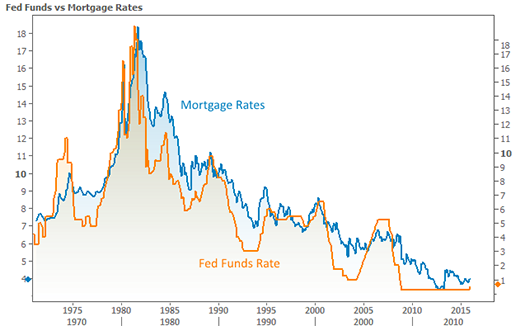

How could we spend the better part of 7 years with the Fed Funds Rate at all-time lows and NOT expect rates to move higher when the Fed ultimately hiked? After all, don’t most interest rates follow the Fed rate over time? The following long term chart of mortgage rates and the Fed Funds rate shows that this is definitely true.

What the chart DOESN’T show—at least not as obviously—are the subtleties that help brighten the outlook. First of all, notice the last Fed hike in 2004. At the time, mortgage rates actually moved slightly lower just after the Fed raised rates. The reasons for that are similar to the present-day reasons.

This all goes back to the Fed providing ample warning for this rate hike. It provided mortgages and other rates the opportunity to move slightly higher preemptively, just like they did in 2004.

The other subtlety is the nature of the longer term trend itself. It’s easier for us to look at this in terms of 10yr Treasury yields, which correlate fairly well with mortgage rate movement over the long run. The longer-term chart shows that the 70’s and 80’s standing out as a potential aberration in the history of interest rates.

Now even the Fed is asking itself what’s “normal” for interest rates. They’ve increasingly pondered the possibility of rates getting permanently stuck in a lower-than-historical range. Fed Chair Yellen also admitted that the Fed would like to raise rates a few times in order to have the means to respond to any adverse shocks to the economy. In other words, part of the reason for raising rates is simply so they have the ability to lower rates again in the future, if needed.

This dovetails with the final subtlety: the short term vs long term economy. In the short term, things are arguably pretty good. Unemployment is low. Job creation is high. There are certainly some nagging issues, but all things considered, we’ve definitely seen worse. In this sense, it’s not an economy that justifies record low Fed rates.

But investors are increasingly wondering when the next downturn will begin gathering momentum. Some see this as early as 2016, though the median view is in the 2-3 year range. The Fed Funds Rate speaks to the short term stability, but rates like mortgages and 10yr Treasuries will take much of their guidance from the longer term economic outlook. Because of this, in conjunction with the other subtleties mentioned above, the Fed rate hike does not doom mortgage rates.

All that having been said, there’s nothing on the other side of that argument that guarantees rates will move lower! As always, rates can move in either direction.

In housing-specific news, the OCC noted an uptick in 30-60 day delinquencies over the past 3 quarters, despite the general improvement in other mortgage performance metrics.

CoreLogic released two reports. The first showed a general increase in mortgage fraud—especially in some areas of the country. The second merely recapped the unsurprising phenomenon of decreasing negative equity, although one interesting statistic might be of use around the water cooler: more than quarter million homes regained positive equity in the third quarter of 2015.

Housing Starts and Building Permits topped analysts’ estimates, thanks to another strong performance from the multi-family sector. A Fannie Mae survey noted an improvement in the outlook for credit availability. And finally, Builder Confidence ebbed slightly, but remains in strong territory overall.